If you have been eyeing Hagerty (HGTY) and wondering whether to get in or wait on the sidelines, the latest move by Oppenheimer offers some food for thought. The well-known brokerage initiated coverage on Hagerty with an “Outperform” rating, highlighting the company’s unique position in the classic car insurance space and its diversified ways of making money. Oppenheimer’s nod could be interpreted as a sign that institutional investors see long-term potential in Hagerty’s approach, or at least recognize the appeal of its loyal customer base.

After this show of confidence from Oppenheimer, Hagerty shares jumped around 6%, marking a noticeable acceleration in trading activity. The stock has gained nearly 30% year-to-date and is up about 19% over the past year. Beyond this recent surge, Hagerty has emphasized its revenue growth and strong rebound in net income, a combination that often catches the eye of investors hunting for durable business models.

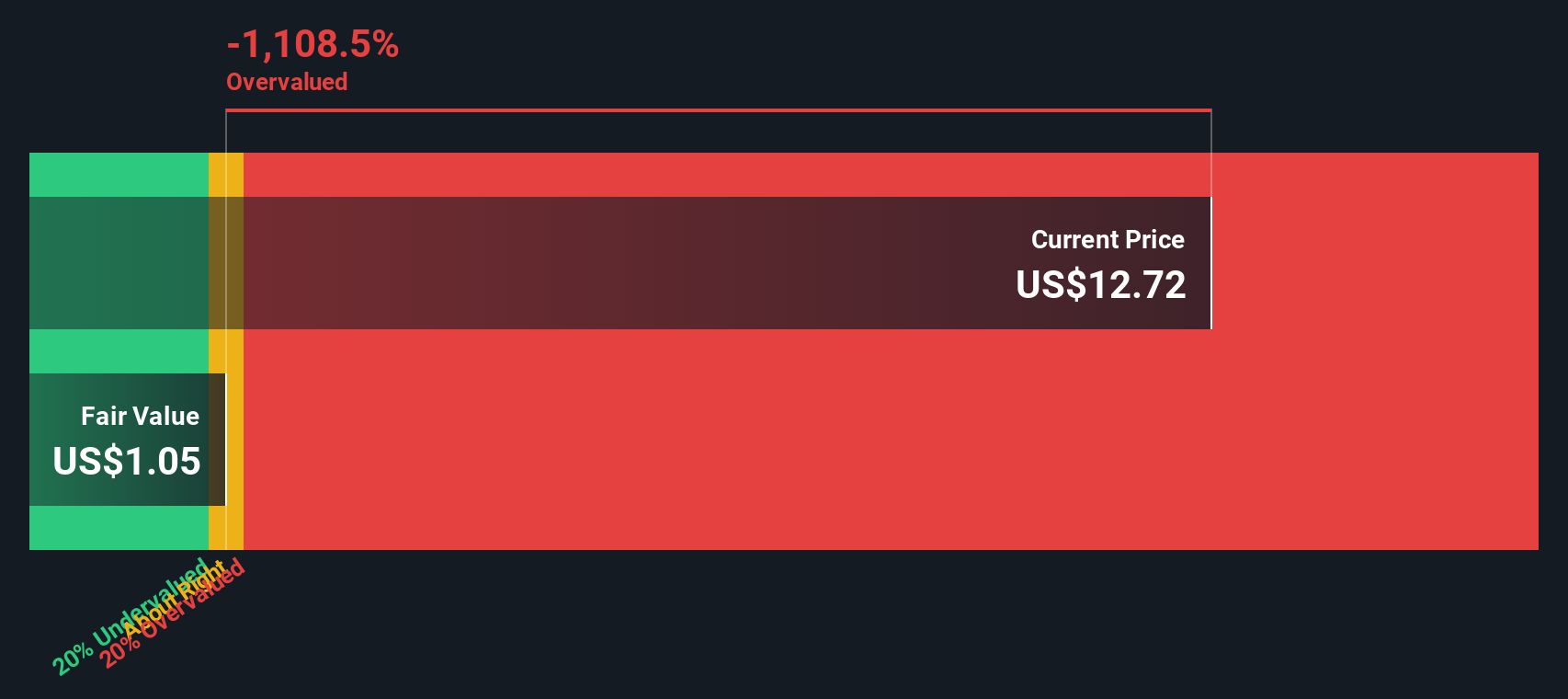

With the stock moving higher on new analyst coverage, it raises an important question: is Hagerty trading at a level that still rewards buyers, or has the market already priced in future growth expectations?

Most Popular Narrative: Fairly Valued

According to the most widely followed narrative, Hagerty stock is trading at a price very close to its fair value. Analysts view the company as priced about right, given its outlook and underlying fundamentals.

The ramping State Farm partnership is expected to significantly accelerate new business growth, providing access to over 500,000 current program vehicles and thousands of motivated agents. This will materially expand Hagerty’s customer acquisition funnel and recurring commission revenues at attractive margins over the next several years.

Curious about the assumptions powering this fair valuation? Discover what makes Hagerty a stock closely watched by analysts this year. A unique mix of partnership catalysts and eye-catching growth projections are at play, revealing bold financial bets shaping the company’s fair value. Want to see which numbers are behind this tight valuation call? Keep reading to uncover the hidden blueprint fueling analyst expectations.

Result: Fair Value of $12.75 (ABOUT RIGHT)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the classic car market’s recent softness and the challenge of attracting younger enthusiasts remain key risks that could pressure Hagerty’s growth outlook.

Find out about the key risks to this Hagerty narrative.

Another View: The SWS DCF Model

Taking a step away from analyst price targets, the SWS discounted cash flow model offers a different perspective on Hagerty. The model suggests the current share price may not align with its long-term cash flow potential. It remains to be seen which approach will influence the market.

Look into how the SWS DCF model arrives at its fair value.

Stay updated when valuation signals shift by adding Hagerty to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Hagerty Narrative

For those who want to dig into the numbers personally and shape the story themselves, it takes just a few minutes to try your own approach: Do it your way.

A great starting point for your Hagerty research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Use your momentum and expand your search. Don’t miss the chance to spot tomorrow’s winners before everyone else does. These strategies could put you ahead of the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Hagerty might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Based in New York, Stephen Freeman is a Senior Editor at Trending Insurance News. Previously he has worked for Forbes and The Huffington Post. Steven is a graduate of Risk Management at the University of New York.