EDITORIAL: There are few divisive issues more contentious than insurance.

There are few divisive issues more contentious than insurance.

It’s something you require and hope you never have to use, but when you need it it can become a non-stop nightmare that drags on that you wish you never had to deal with.

With Alberta having the second highest average premiums in the country – Ontario takes a back seat to no one – reforming and fixing the auto insurance model in the province needs to be a core mandate of the provincial government.

When mandate letters were given by Premier Danielle Smith to ministers, the affordability and utilities ministry was tasked with giving short- and long-term recommendations for car insurance.

Smith introduced a 3.7 per cent annual hike cap for good drivers and highlighted long-term plans were soon-to-come.

It released a pair of studies about two months ago on adopting different insurance models and what, if any, economic impact may happen. Those insurance models ranged from a public auto insurance model, maintaining the status quo and having more private sector involvement.

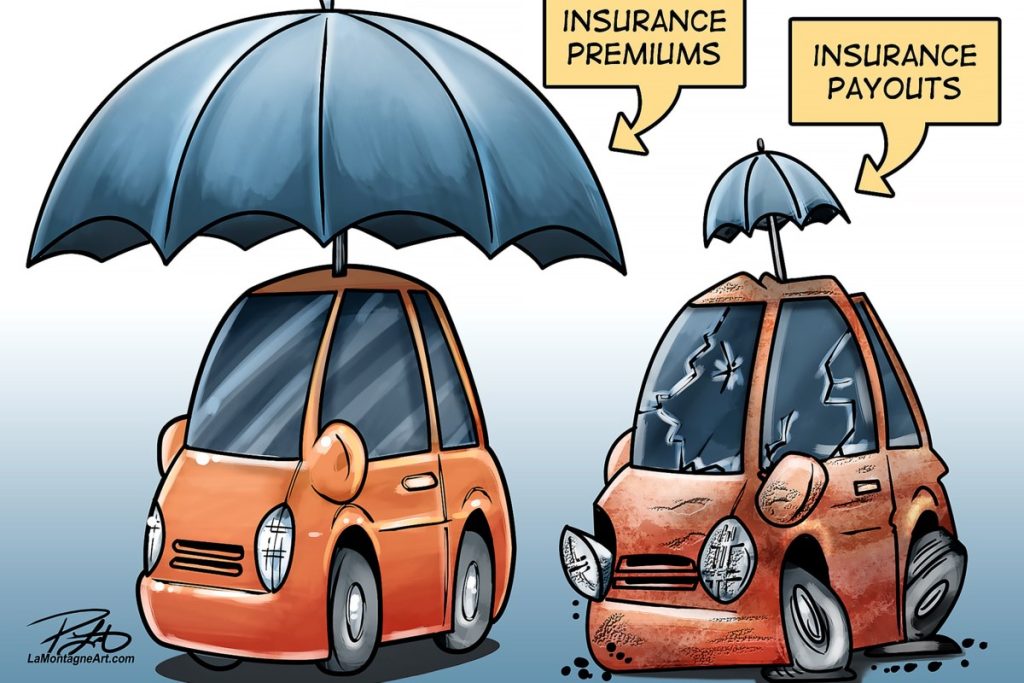

As part of the studies, it found an average of five per cent of Albertans’ disposable income went towards auto insurance. A Fraser Institute 2011 study had it at 2.7 per cent and insurance premiums have only continued to climb from an average of $1,316 in 2018 to $1,670 in 2023.

One of the provincial-commissioned studies found full coverage in a public auto system could average less than $1,000 a year. One of the key aspects to lowering costs in public systems in Manitoba, Saskatchewan and British Columbia is removing the ability to sue and claims are handled by the insurer.

The last provincially-commissioned study in 2020 on insurance reform called for Alberta to take on a no-fault compensation model, though then Premier Jason Kenney and former Finance Minister Travis Toews balked at any meaningful change.

A cap for good drivers is an easy place to start – and rightfully so – since people with impeccable driving records shouldn’t be penalized. However, some insurance companies have already found a temporary way around the cap, depending on when they file rate changes with the province meaning it could be 2025 for some drivers.

As of June 10, the Automobile Insurance Rate Board – an independent agency that regulates Alberta’s insurance – the average premium increase for people who qualify as bad drivers is about 13 per cent.

The increase is far above inflation and likely more than the majority of people can afford without making drastic cuts elsewhere in their finances.

The provincial government asked people to provide feedback before June 26, but after fiascos in which it sought feedback from the public on municipalities with Bill 20 and then largely ignored people, skepticism about what the province may do with the engagement is understandable.

As much as people may dislike auto insurance, it is necessary. And while people want to pay as little as possible, coverage literally comes at a cost for potential health care from a collision, vehicle repairs and protection against possible lawsuits.

Few people are likely to read their annual insurance notice or even understand what it is they pay for, but much of the coverage is crucial for anyone who owns a vehicle.

Regardless of the outcome of the public consultation, the provincial government can’t sweep residents’ wants and needs under the rug as they’ve shown they prefer to do.

Instead, a meaningful and thoughtful reform of the auto insurance field needs to take place in Alberta.

For a government that touts affordability as a main priority, anything less than systemic changes to auto insurance in the province is unacceptable.

Based in New York, Stephen Freeman is a Senior Editor at Trending Insurance News. Previously he has worked for Forbes and The Huffington Post. Steven is a graduate of Risk Management at the University of New York.