Economics Matters — Blog/Podcast/Financial Riddler/MaxiFi Puzzler

Sign up for a free subscription at larrykotlikoff.substack.com. I’ll immediately make it a free lifetime subscription. Also, pls sign up kids, parents, …, everyone you know.

Paid subscriptions come with a monthly Q&A session via Substack Live. I’ll email you the day and time. Submit questions on anything and everything via chat. I’ll be live. Subscribe as a Founding Member – Help me provide high-level economics content and break even covering my significant podcast costs. Comes with a one-hour financial therapy session (kotlikoff@gmail.com) and full access to my monthly Q&As sessions.

Teaching Financial Literacy/Economics at any level? Email me for free MaxiFi licenses for your students and a free PRO license for yourself. kotlikoff@gmail.com Speaking Inquiries — visit www.chartwellspeakers.com

A month ago, a German court ruled that Google was liable for damages arising from its AI-generated statements. Here’s the Yahoo.com headline:

Germany told Google it owns every wrong answer its AI gives — and 78% of Americans already use these tools

Clearly, most of us now use AI for mundane things, like checking the weather. But some two thirds of us also use it for financial advice. If you’re one of the two thirds using AI for money matters, here’s my advice:

DON’T

If you click here, here, here, here, here, and here or you just keep reading, you’ll find case studies where AI delivers bad to awful financial advice. Moreover, the different AIs produce different bad to awful advice. Indeed, the same AI can deliver different bad to awful advice just by using different phraseology in one’s prompt. Or it may, as it tried to do with me, calculate its advice based on the method it thinks its user most prefers.

I’m of course, an economist who has an economics-based financial planning software company that markets MaxiFi Planner. The AIs recognize my name from my email address and deduce they should try to apply economic principles to financial planning rather than rely on its training set — Wall Street’s profit-motivated, conventional financial-planning methodology.

Whether it’s providing saving, spending, or insurance recommendations or telling you how to optimize your Social Security benefits, do Roth conversions, or handle retirement account contributions, conventional planning delivers recommendations at major, if not total odds with economics-based financial advice.

Next the AIs tell me that to do things even approximately right (their candor is charming) will require hours if not days. Fortunately, running AIs from incognito windows and telling them to assume they are interacting with a random person led them to produce their standard insurance “advice,” what they openly admit they would tell their standard user.

Easily-Calculated Rules of Dumb Don’t Cut It, But the AIs Can’t Even Agree on the Wrong Answers.

Consider your life insurance needs. Economics says hold enough to ensure your survivors can maintain the same living standard as would occur were you not to die. That’s a complex calculation. You need to figure out your family’s living standard if you don’t pass. This requires taking account of a host of interrelated issues including your current regular and retirement assets as well as your future earnings, retirement account contributions and withdrawals, special expenses on healthcare, etc., housing expenses, estate plans, federal and state taxes, IRMAA Medicare Part B premiums, Social Security benefits, Roth conversions, requisite life insurance premiums, the tax and IRMAA codes incomplete and, in some large parts of our tax code, no adjustment for inflation.

To make matters worse, you need to think through your survivors’ situation. I.e., you need to do what MaxiFi does — contingent life insurance planning and ask, “If I die, how much will my spouse earn?” “Will they adjust their housing? “Will they downsize and relocate to a different, low-tax state?” “And how much will they pay in taxes with me out of the picture?” “Also, what will they receive in Social Security survivor benefits.”

Demographics matter as well. How many kids do you have and when will each leave home? How long could your spouse live? Are any of your children disabled? Finally, are your kids as expensive as adults, and how much less will your spouse need to spend with one less mouth — your mouth — to feed? I.e., what are your economies of shared living.

Deciding what to do if no one dies early and what will happen conditional on each spouse/partner dying in each future year is tough sledding. More challenging yet, one eeds to make sure that all these calculations line up. In particular, one needs to account for the following chicken and egg (simultaneity problem): The amount of insurance needed depends on the per person living standard to be insured. But those insurance premium payments impact what living standard can be sustained in the case no one dies early, which impacts the living-standard target for survivors, which influences how much life insurance is needed and premiums paid, which influences …

Answering these questions requires writing down complicated, intertwined, non-linear equations — ones that handle all the above issues and more — and solving them simultaneously. This is what MaxiFi Planner, does — in three seconds, producing results that users can see, at a glance, are internally consistent and fully correct. For example, one confirm that the household members’ annual living standards if neither the household head or spouse/partner dies young is, to the dollar, the same as that of survivors regardless of the date of a premature death. (This eyeball proof requires flipping a switch to permit borrowing in cases the household or survivors are cash-flow constrained.)

MaxiFi is the only planning tool that gets this right because its the only economics-based planning tool on the planet. I wish there were others. Then I could avoid the apparent conflict-of-interest in comparing economics’ financial recommendations with those of Wall Street — recommendations based on profit-oriented, ad hoc shortcuts that even an AI can replicate. Indeed, the industry’s actuaries, none of whom appear to have an advanced degree in economics, have developed five different simple, as in, this can be programmed in Excel, methodologies:

-

Multiple‑of‑income approach (10× income rule)

-

DIME method (Debt, Income, Mortgage, Education)

-

Human Life Value approach (income‑replacement present‑value model)

-

Capital needs analysis

-

Capital retention analysis

AI, is trained to spit back answers based on its training data, which overwhelmingly comprises industry “advice.” The old expression, garbage in, garbage out, could not be more appropriate. Moreover, AI can now run spreadsheets meaning agentic AI tools can now replicate the same inappropriate calculations being preformed by all the life insurance companies, large and small.

But the big take away form this list of five methods is that there is more than one method. There is only one question and only one proper method to answer the question that arises with respect to life insurance — what’s needed to preserve survivors’ living standards.

Suppose an AI recommends far too little coverage for a husband named Joe, where far too little references leaving survivors unable to maintain their living standards. Further suppose that Joe prints out his AI’s advice and buys exactly what it recommends. Next assume that Joe strokes out the next day. When his wife Sally realizes Joe left her and the three kids with far too little life insurance, she’ll surely march straight to Luddites, LLP, Attorneys at Law or whatever law firm is suing the AI industry on a class action basis and sign up.

If the AI company says its recommendations just follow industry standards, a jury may say, “Sorry, you should have followed best practice in determining life insurance needs, namely what economics says — insure survivors’ living standards. You’re inability to calculate those living standards in an internally consistent way — when the software for doing so was and is available for your immediate use and costs next to nothing — is no different from prescribing/recommending a completely ineffective herbal supplement for a staff infection because you don’t manufacture antibiotics.”

I told three AIs — Perplexity, ChatGPT, and Claude Pro — to calculate the life insurance needs for a 50 year-old husband making $100K with a low-earning wife and three kids. My exact prompt, which includes all the inputs I entered into MaxiFi, is copied below. Each AI used the Capital Needs Analysis method, which is one of the industry’s rule-of-dumb methodologies. Spending needs under this method are based on what the household is currently purchasing on a monthly basis. But using this amount makes no sense. It may be far higher or far lower than the sustainable amount. Alternatively, spending needs are based on multiplying the households annual gross income by 70 to 80 percent. In contrast, as stated, MaxiFi computes, in an internally consistent manner, the household’s spending under two restrictions. First the path of spending must be affordable. It must remain within the household’s lifetime budget. Second, annual spending must be set to sustain the household’s living standard per household member through time subject to cash-flow constraints.

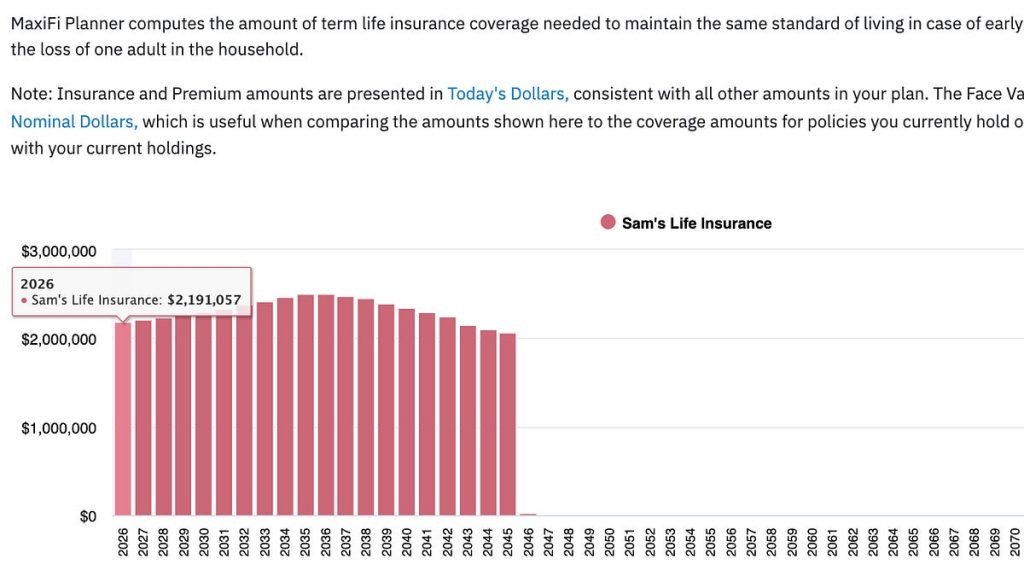

The chart below shows MaxiFi’s answer. The husband needs $2,091,057 in life insurance this year. His required insurance peaks in 2035 at $2,504,005. These and the other values are the annual amounts requried to provide his wife the resources she needs, in present value, to afford, to the dollar, the same annual real living standard she and her children would enjoy were the couple to live to their maximum ages of life.

The insurance amounts rise through 2035 because the present value of the husband’s age-70 (year 2046) inheritance, which is contingent on his survival, increases. Intuitively, as the year 2046 becomes closer, the present value of the inheritance rises — the inheritance that will go poof if the husband dies before 70. After 2035, this force is still at play, but there is a countervailing factor lowering the husband’s insurance needs — he has fewer years of earnings left to insure.

As you can see, Perplexity advises the husband to purchase $1.3 million, which is far short of the $2.2 million that’s needed. Indeed, it’s roughly one third of what Claude Pro recommends.

ChatGPT’s 2026 recommendation is close to MaxiFi. But by 2036, it’s less than half of what MaxiFi recommends.

In making its calculation, Claude Pro said: “This is a genuinely complex actuarial/financial-planning calculation — it needs Social Security survivor-benefit estimation, career-earnings-based PIA calculations, and year-by-year present-value modeling.” Ten minutes later — not MaxiFi’s 3 seconds later — Claude reported the husband should purchase $3.82 million in life insurance coverage this year. That’s almost twice what MaxiFi says is needed! Claude gets that the husband’s coverage needs to rise with age, but coverage peaks too late and continues beyond age 70 when no coverage is needed.

Clearly, AI is not ready for prime time when it comes to providing life insurance or any other financial advice. Three of the leading AIs are producing wildly different recommendations in this example and none closely accords with what economics and common sense suggests — insure the living standards of survivors. But here’s the rub. Determining life insurance needs on this appropriate basis requires, to repeat, calculating the household’s living standards absent premature death. Doing so correctly, let alone instantly, requires decades of advanced programming and algorithmic development — not training a predicting machine on the wrong answers and having it guess what to do and how to do it. This said, AIs can be trained using MaxiFi to convey appropriate life insurance and other economics-based financial advice. Whether the AI companies will seek such training remains to be seen.

What term life insurance amounts do I need in each future year, valued in today’s dollars? I’m 50. My birthday is 6/1/1976. My maximum age of life is 90. I make $100K a year. I will work through and including age 67. My salary will keep up with inflation. I have a military pension that will pay $50000 a year in today’s dollars starting at age 60. The pension has no survivor benefit. I started working at age 20, earning $45,000 a year. My salary grew at 4% annual through last year. My wife’s birthday is 6/1/1986. Her maximum age of life is 100. She earns $25,000. Her salary will keep up with inflation. She will work through the year 2048. Her first job was at age 20 when she earned $15000. Her salary grew through last year at 2% a year. She will stop working entirely if I die. We are planning assuming inflation runs at 2.25% annually going forward and that we will receive a 4.75% return on all our regular and retirement account assets. We have three children. One was born on 6/1/2010, one was born on 6/1/2015, and one was born on 6/1/2020. Each will leave home on January 1st of the year they will turn 19. We live in Georgia. We have a house worth $500,000 that we don’t plan to sell. Annual property taxes are $5000. Annual homeowners insurance cost $5000. Annual maintenance cost $10,000. These costs will rise with inflation as will the value of our home. We have $150,000 in our savings account. My 401(k) assets total $350,000. My employer and I each contribute $6000, measured in today’s dollars, annually to my 401(k). My wife just inherited a $250,000 inherited IRA that she received at the end of last year. She is, starting this year, withdrawing the same real amount each year starting this year. My wife will take her Social Security retirement benefit at 62. I will start my retirement benefit at age 70. We will file for all Social Security spousal and child benefits that might be available. At 68, I will start withdrawing the same real amount each year from my 401(k). I will receive a $2 million inheritance at age 70. If I die before age 70, it will go to my sister. I can’t borrow.

Clinton Mora is a reporter for Trending Insurance News. He has previously worked for the Forbes. As a contributor to Trending Insurance News, Clinton covers emerging a wide range of property and casualty insurance related stories.